Title

Applied Econometric Time Series,Used

Sold by Ergodebooks, an authorized reseller.

Returns accepted within 30 days | support@ergodebooks.com

Shipping Information

- Free Standard Shipping — United States only

- Processing Time: 3–5 business days

- Estimated Delivery: 6–10 business days after dispatch

- Double-boxed, fully insured & discreetly packaged

- Tracking number sent via email once dispatched

Returns & Refund

Returns accepted within 30 days of delivery.

Damaged or Defective Item

Free return shipping + replacement or full refund

Wrong Item Received

Free return shipping + replacement or full refund

Change of Mind

Return shipping at customer's expense · 25% restocking fee applies

Payment Option

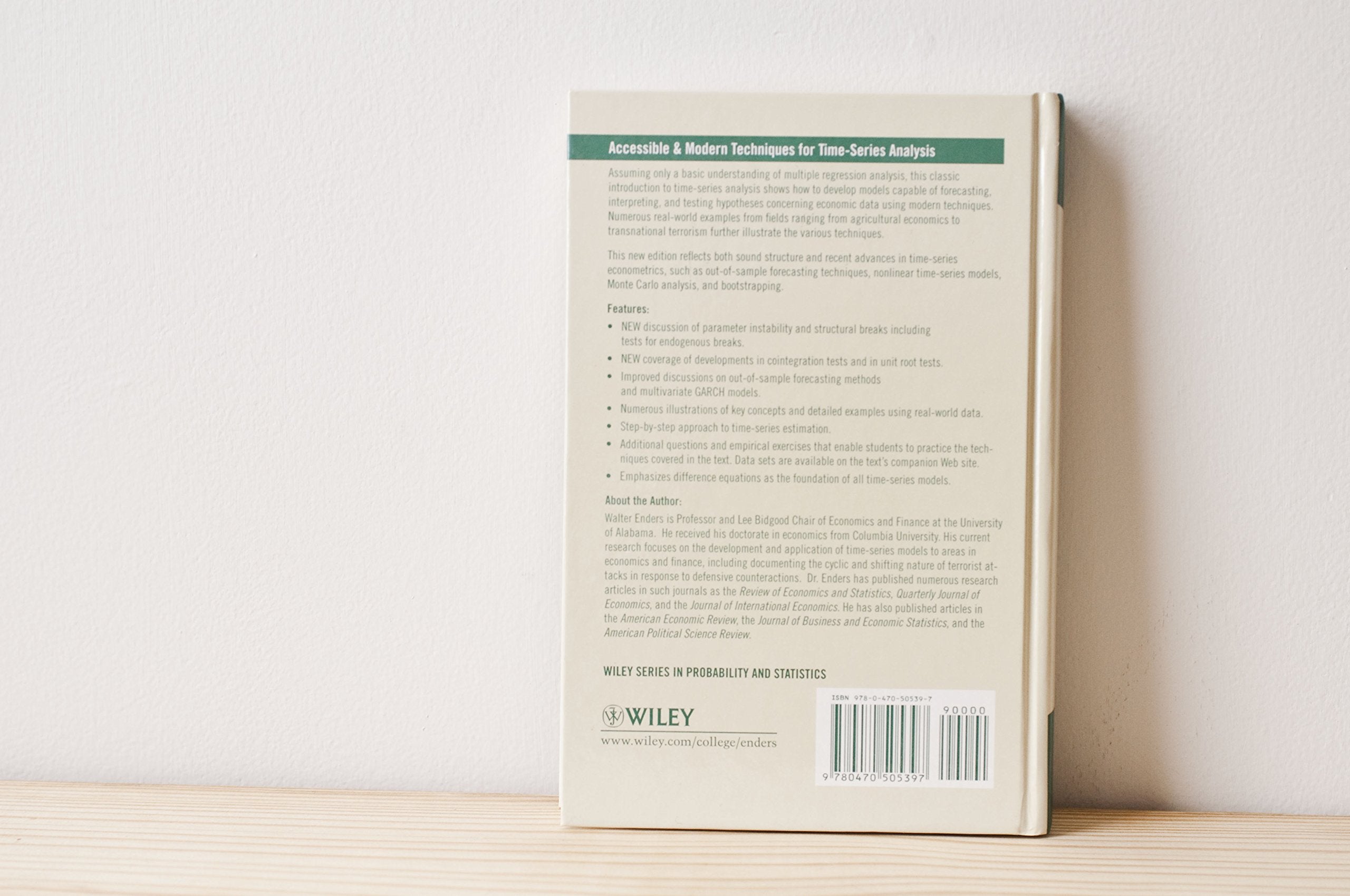

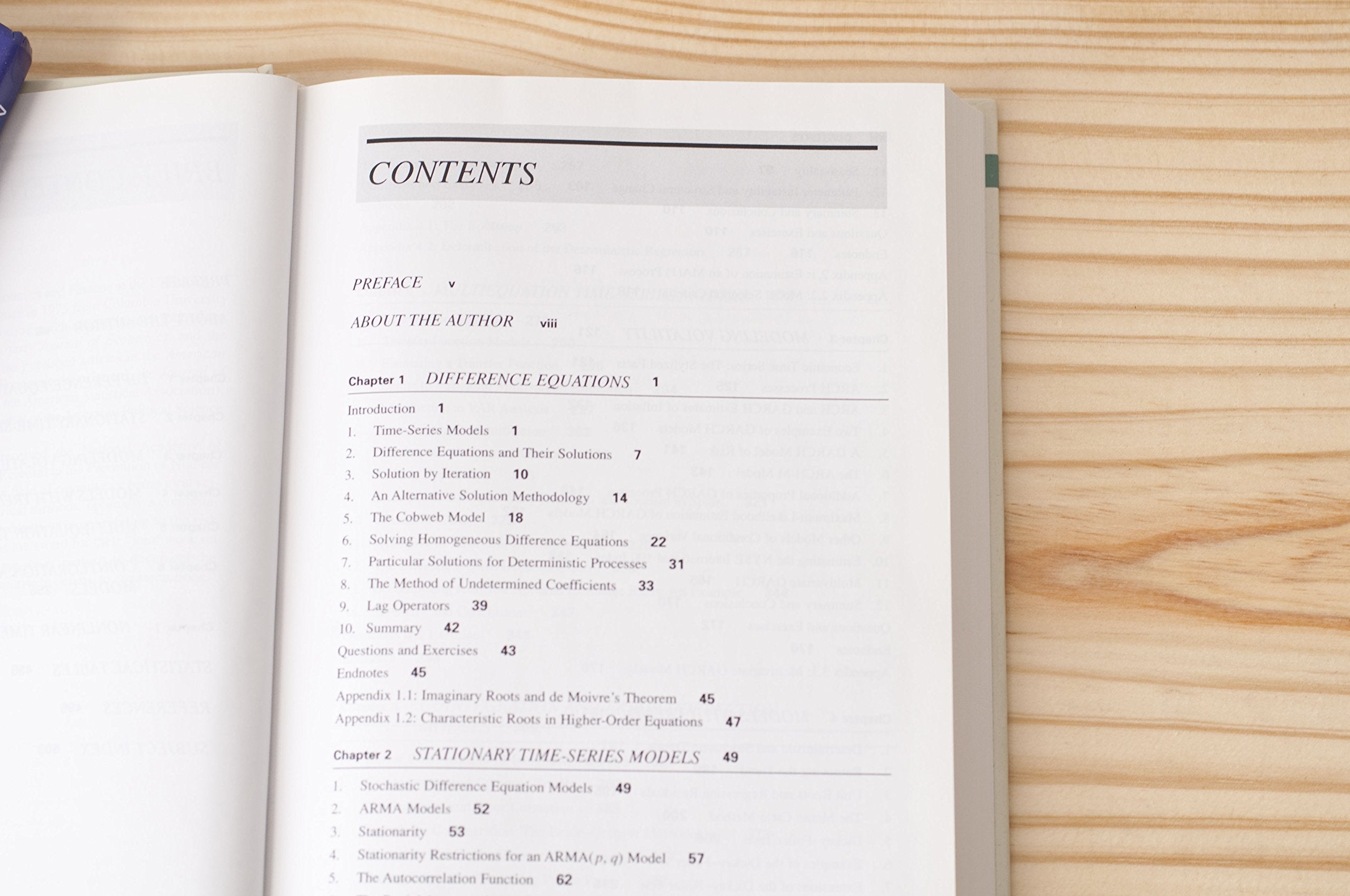

Enders continues to provide business professionals with an accessible introduction to timeseries analysis. He clearly shows them how to develop models capable of forecasting, interpreting, and testing hypotheses concerning economic data using the latest techniques. The third edition includes new discussions on parameter instability and structural breaks as well as outofsample forecasting methods. New developments in unit root test and cointegration tests are covered. Multivariate GARCH models are also presented. In addition, several statistical examples have been updated with realworld data to help business professionals understand the relevance of the material.

⚠️ WARNING (California Proposition 65):

This product may contain chemicals known to the State of California to cause cancer, birth defects, or other reproductive harm.

For more information, please visit www.P65Warnings.ca.gov.

- Q: What is the main focus of 'Applied Econometric Times Series'? A: The book provides an accessible introduction to time-series analysis, emphasizing model development for forecasting and hypothesis testing in economic data.

- Q: Who is the author of this book? A: The author of 'Applied Econometric Times Series' is Walter Enders.

- Q: What is the publication date of this edition? A: This edition was published on January 1, 2009.

- Q: How many pages does the book have? A: The book contains 517 pages.

- Q: What are some key features of the third edition? A: The third edition includes discussions on parameter instability, structural breaks, out-of-sample forecasting methods, and updated statistical examples with real-world data.

- Q: What is the condition of the book? A: The book is classified as 'Used Book in Good Condition'.

- Q: Is the book hardcover or paperback? A: The book is a hardcover edition.

- Q: What topics in econometrics are covered in this book? A: The book covers unit root tests, cointegration tests, and multivariate GARCH models.

- Q: Who would benefit from reading this book? A: This book is designed for business professionals and students looking to understand time-series analysis and its applications in economics.

- Q: Is this book suitable for beginners in econometrics? A: Yes, it is written to provide an accessible introduction, making it suitable for beginners in econometrics.