Title

Portfolio Optimization (Chapman and Hall/CRC Financial Mathematics Series),Used

Sold by Ergodebooks, an authorized reseller.

Returns accepted within 30 days | support@ergodebooks.com

Shipping Information

- Free Standard Shipping — United States only

- Processing Time: 3–5 business days

- Estimated Delivery: 6–10 business days after dispatch

- Double-boxed, fully insured & discreetly packaged

- Tracking number sent via email once dispatched

Returns & Refund

Returns accepted within 30 days of delivery.

Damaged or Defective Item

Free return shipping + replacement or full refund

Wrong Item Received

Free return shipping + replacement or full refund

Change of Mind

Return shipping at customer's expense · 25% restocking fee applies

Payment Option

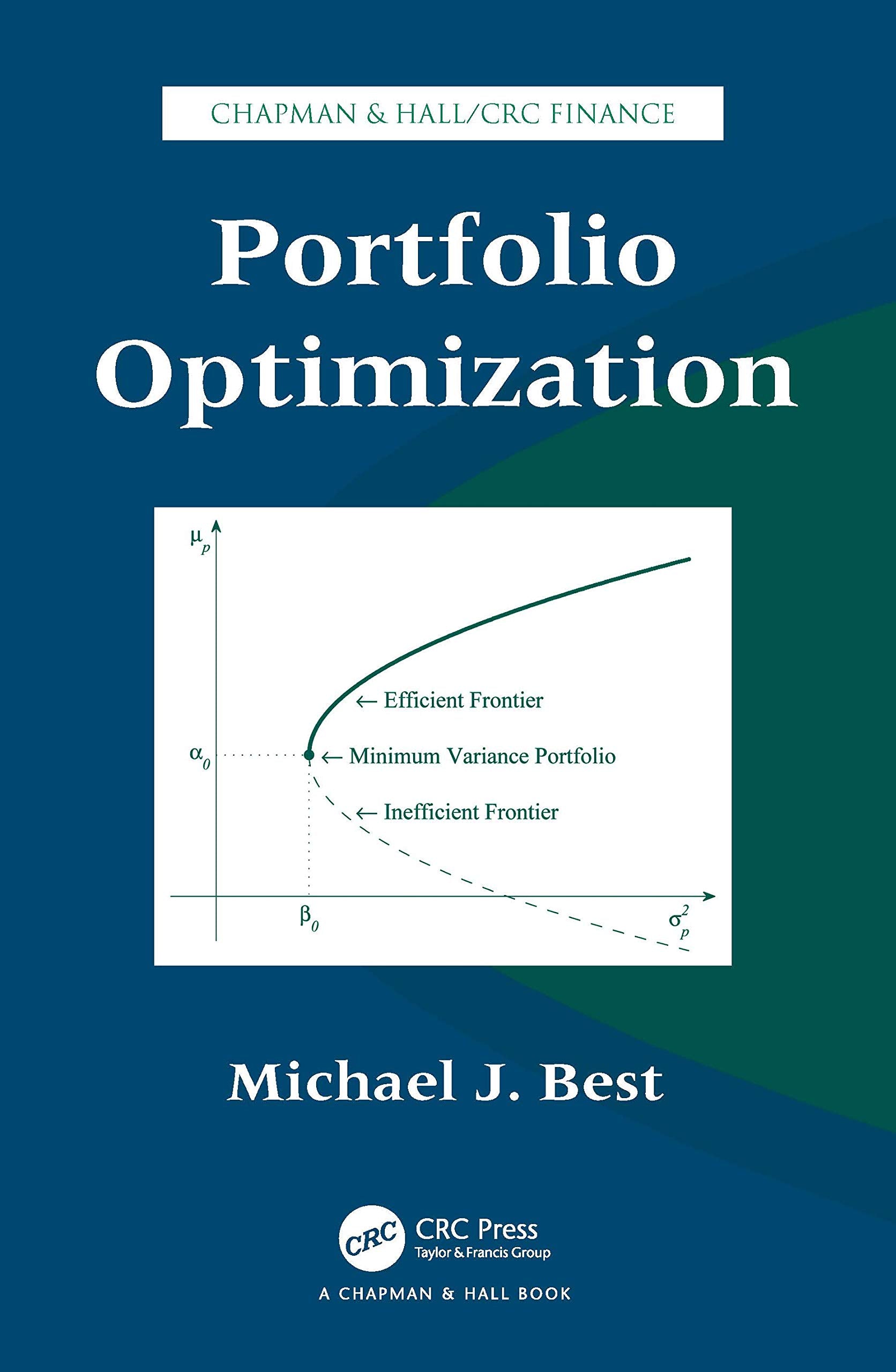

Eschewing a more theoretical approach, Portfolio Optimization shows how the mathematical tools of linear algebra and optimization can quickly and clearly formulate important ideas on the subject. This practical book extends the concepts of the Markowitz "budget constraint only" model to a linearly constrained model. Only requiring elementary linear algebra, the text begins with the necessary and sufficient conditions for optimal quadratic minimization that is subject to linear equality constraints. It then develops the key properties of the efficient frontier, extends the results to problems with a riskfree asset, and presents Sharpe ratios and implied riskfree rates. After focusing on quadratic programming, the author discusses a constrained portfolio optimization problem and uses an algorithm to determine the entire (constrained) efficient frontier, its corner portfolios, the piecewise linear expected returns, and the piecewise quadratic variances

⚠️ WARNING (California Proposition 65):

This product may contain chemicals known to the State of California to cause cancer, birth defects, or other reproductive harm.

For more information, please visit www.P65Warnings.ca.gov.